DB Wood Team

4th August, 2017

Blog, Hot Topics

Tax Returns: The Present & Future

Following the Spring Budget, Philip Hammond revealed his policy to reduce the relatively new dividend tax allowance from £5,000 to just £2,000 as of April 2018 (make your mind up for goodness sake). Roll back to 2015/16 and you could potentially have earned a whopping £42,385 in total gross income before paying any further dividend tax… quite a change! (Source: HM Revenue & Customs, 2015)

The objective of introducing the dividend allowance was to reduce the tax effectiveness of dividends, and at the same time to encourage small business owners who pay themselves predominantly in dividends, to convert to the traditional pay as you earn (PAYE) taxation method that most employed people are familiar with. This is a more efficient way for the government to collect tax, and it is instantaneous, rather than deferred. Dividend tax is paid 50% in the year of receipt, and the balance the following tax year.

So, the new dividend allowance is a major sea change, and dramatically affects the tax paid by several business owners. It sits alongside the Revenue’s other suite of allowances such as the personal allowance, and if you exceed any of them, the chances are you will need to pay some tax.

The reduction in dividend tax allowance between this tax year and next will affect around 2.27 million people, causing an average tax increase of £315 and a rapid increase in the number of tax returns that need to be submitted! Overall it will bring the Treasury an estimated £1bn through extra taxes (Source: The Telegraph, 2017).

If you have an investment portfolio, this allowance might also effect you….

If you hold an investment tax wrapper called a “Personal Portfolio” or Open Ended Investment Contract (OEIC) or even shares or bank account savings, these can produce both dividends and interest as part of its investment return. Whilst it is our job to use your various allowances where available, there will soon be less to use, and so investors who have not needed to report these sources of income in the past may now have to.

How will I know if my dividends/savings from my “Personal Portfolio” are going to be more than £5,000?

Standard Life will automatically generate a consolidated tax certificate from the Standard Life WRAP platform, which the DB Wood team will review and notify you if there are any actions that need to be taken (such as completing a tax return).

The future of tax returns- the good news:

The Government plans to automate the reporting between HMRC and the investment provider through new digital tax accounts from 2020, removing the onus on the individual to report the income themselves.

The future of tax returns – the bad news:

The shiny new system is still in design stage, so it will be several years before we get to report any taxes in the digital tax accounts. In the meantime, it is down to individuals to report income themselves where tax has not already been deducted at source such as salary.

Conclusions:

More and more people will now have to declare certain income and savings than ever before. It is our job to use your allowances where possible, and where not, we will notify you if further action is required. Potential actions should in theory get easier in the future, but let’s wait and see the final outputs before we jump on the digital tax bandwagon.

If you’re interested in knowing more about the different tax allowances, and potential actions, we have compiled a Q&A to help…

Appendix:

What is a tax return and do I need to complete one?

A tax return is the current reporting method for informing HMRC how much income and capital gains you have made during a tax year. It is generally required annually, when you have income that is not fully taxed at source, for example if you are a landlord receiving rent or you have sold a large investment which has made a capital gain.

How do I submit a tax return?

Complete a Self-Assessment tax return and submit it to HMRC. Don’t be late though! If you miss the deadline, you will have to pay a penalty fee and interest on any tax owed!

My dividends are above £2,000 and/or interest over £1,000, what do I need to do?

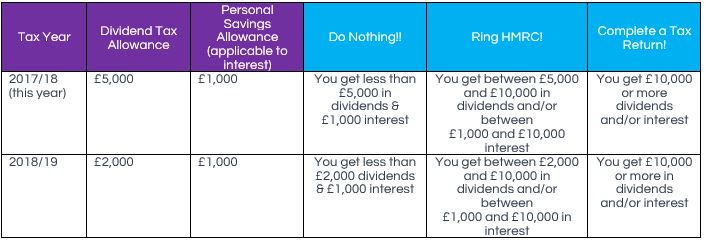

As we like to keep things simple and fun, we have created a table to show you what you may need to do:

As the table shows, there are 3 possible outcomes:

- If your dividends/savings income are in the “Do Nothing!!” column, no action needs to be taken – hurrah!

- If your dividends/savings income falls within the “Ring HMRC!” column, a simple phone call to HMRC is all that is needed. HMRC will then arrange for any tax to be automatically collected from other income sources such as your salary.

- If your dividends and/or savings income fall in the “Complete a Tax Return!” column, you will need to complete and submit a Self-Assessment Tax Return.

What counts as dividends or savings income?

Dividends from shares or collective investments that are not wrapped in an ISA will count as dividend income. Bank account interest, interest distributions from collective investments that aren’t wrapped in an ISA and interest from Government and Company bonds will all be classed as savings income.

The DB Wood Team are always on hand to help with any queries you may have and we hope you find this article useful for your own understanding. Please don’t hesitate to contact our team.

References:

HM Revenue & Customs (2015), “Income tax personal allowance for those born after 5 April 1938 for 2015-16”. Available at: https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/385235/Personal_Allowance_for_2015-16.pdf (Accessed: 17th July 2017)

The Telegraph (2017), “Dividend crackdown: ‘a tax on widows’”. Available at: http://www.telegraph.co.uk/investing/shares/dividend-crackdown-tax-widows/ (Accessed: 14th July 2017)