Ashley Brooks

13th October, 2017

IC Insights

Investment Review Quarter 3 2017

Market Review of Quarter Three

The summer of 2017 may be remembered as a turning point in this economic cycle. After a decade of pumping money into developed economies, Central Banks look to have put that policy in their rear-view mirror, signalling that interest rate hikes are likely to be sooner rather than later.

Investment markets were looking to Central Banks and economic data for direction through the summer months, hoping both would point the way to improving growth and rising inflation. To be fair, economic data over the summer was pretty positive. We do seem to have growth all over the globe (synchronised global growth is the new buzz phrase) but much of this growth is at low levels. Further, wage inflation is not showing anything like sufficient momentum to suggest that consumer spending is likely to rise anytime soon. The worry is that if interest rates rise too fast, and consumers are hit in their pockets, then we could quickly hit the slippery slope towards recession. We don’t have big margins.

Markets have been trying to trade-off the positive economic data with the concern of policymakers taking off their harnesses. Understandably, the results have been mixed – global equity markets were up around 4% in August, but then sold off to end the quarter up just 1.5%. They were led higher by Europe and Emerging Markets (areas we have been overweight), with Japanese and US markets lagging (Financial Express, 2017). Other asset classes also struggled to gain traction; bond markets in the UK lost value after they became concerned about Mark Carney raising interest rates in November. The trend was similar across the globe as well, with the IA Global Bonds benchmark posting a small negative return overall (Financial Express, 2017). Finally, our Absolute Return exposure produced just that – a small absolute return.

One area that continues to offer some sustainability however is UK Commercial Property. It has offered more than 5% year-to-date and more than 2% in the last quarter. Despite Brexit fears, overseas demand for property remains strong with the pound still cheap vs history. It is even more interesting given the fact that the UK economy appears to be stalling. Inflation has hit 2.9%, its highest level since 2014, and with wage growth still below that level, the UK consumer is waning. Then again, I heard an interesting comment the other day that “cities will soon hold more power than countries”, but that’s another blog all-together. Crucially, it’s one of the only areas that continued to offer a sustainable income through Q3, despite the backdrop.

Outside of Central Banks, politics once again took centre stage with the objective of fright. Investment markets don’t seem overly concerned about the spat between North Korea and Trump. They tend to think that the rhetoric from both is just hot air, on the basis that no one is stupid enough to press the button. Let’s hope so! Nonetheless, a watchful eye on our political figures is required.

This quarter reminded us (in case we needed it), that the only certainty is uncertainty. The policy landscape has changed – it’s not a question of how but when the effects come through to markets, though it might take two months or two years to fully play out. It’s at times like these that we remind ourselves how hard it is to predict and foresee the risks out there – the second you feel you have everything covered is the second you are most at risk. To this end, some modesty and risk control can go a long way.

Portfolio Review

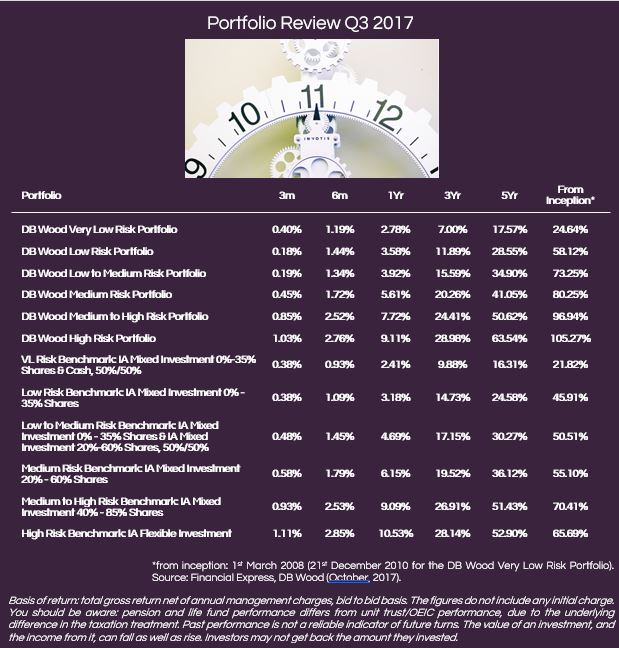

Against that backdrop, the portfolio range added between 0.18% and 1.03% across the quarter, taking the year-to-date returns to between 2.39 and 6.63% depending on the risk profile selected.

Overall, that puts us in line with benchmarks in 2017, despite operating with significantly less risk across the range. To reaffirm however, we operate our investment strategy quite differently to benchmarks, and really measure ourselves against the return targets we set over a rolling five-year time horizon (detailed below). Our objective is to take as little risk as possible to achieve those, maximising the chance that our clients’ financial plans work and their objectives can be met.

The five-year horizon doesn’t mean we are not active in the way we manage the models however – as discussed before, it is crucial to continue to review risks and opportunities. In fact, we have already made four such portfolio changes across the year, the last being in August. Here we continued to add to our convictions in certain bond areas, tilting the portfolio to perform better if economic data picked up (as we expected), and tweaked up exposures to UK Commercial Property and Japanese equities.

We also remain very positive on the long-term story in Europe and Emerging Markets, with those overweight positions rewarded in Q3. Outside of that, it was consistency that was the name of the game, as all components combined to provide a steady journey through a difficult environment. Even our bond allocation contributed positively, despite overall indices offering a negative return over the summer.

Our strong end result is even more surprising given the poor performance of our biggest equity holding across Q3; Woodford Equity Income. Various unrelated issues caused a poor quarter for Neil Woodford and his team, as the fund underperformed significantly. Importantly, our size and scale now allows us unparalleled access to fund management groups, so we kept in close contact across the period to fully understand and monitor developments. We have not taken the decision to sell the fund, and remain highly convicted to Neil’s philosophy over the longer term.

It feels like an eternity ago that we were discussing a negative outlook for gilts (UK Government Bonds) after their stellar run in 2016. We have held close to 0% here since that time, citing various risks to an eye-wateringly expensive asset class. In just eight days in September, the Bloomberg Barclays Sterling Gilts Index fell 3.5% – not quite the behaviour you expect from a “risk-free” asset. Avoiding risks such as this is just as important as participating in the best opportunities – sometimes the things you don’t buy can provide a greater benefit than the things you do.

In summary, the portfolios did exactly what we would expect them to do in a challenging environment; navigate through smoothly.

Market Outlook

Our expectation is that global growth is now sufficiently self-sustaining to handle reduced financial stimulus from Central Banks. The timing of interest rate rises is probably the biggest risk though, but if applied correctly, they may support and extend the current rise in equity markets.

The risk of a policy mistake or a political upset disrupting markets remains. With public and private debt levels very high, geopolitical risks are also elevated. If Central Bank policy is not sensitive to economic conditions, we could see a big sell off, not just in equity markets but also in bonds. These are without doubt, reasons to remain cautious.

Focusing on the UK; a reversal of the 0.25% interest rate reduction (following Brexit) seems likely, though it will be important to pause for a while to take a view on how the economic landscape adjusts before amending rates further.

On the Brexit front, there has been little progress in resolving issues such as EU citizen rights, the exit bill and the Ireland border that are preconditions for moving on to discussing the UK’s future relationship with the EU. The most recent signals are that positions are hardening. The pound continues to ebb and flow due to the combination of Brexit negotiation and weak leadership. Our politicians are doing little to instil confidence.

Specifically looking out to December in the US, we also have the fight over raising the US debt ceiling to be decided. Add in the potential for some US tax reform and you have two events out of the US that could direct things from here. Of the risks that we can see, this is where our attention is focussed.

With the risks covered, it is important to contrast that there are lots of reasons to be cheerful. Companies globally are reporting higher than anticipated earnings, and in the US, we are starting to see some signs of wage inflation. All this would point to an extension of equity market returns, but then valuations are already very high (on average). It is difficult to see that returns are going to be significant moving forward. In our view, return expectations need to continue to be managed downwards. We favour value stocks within our equity exposure, and therefore it will be important to remain under exposed to passive indices where inflows continue at a significant pace, effectively herding people into stocks without good justification. If a correction were to come, diversification through effective stock picking will be key to maximise the opportunity of buying back in.

In fixed income, there is very little opportunity other than in Emerging Markets. The income returns elsewhere are low, and capital loss is very likely if interest rates increase faster than markets anticipate. We are therefore only holding very short-term fixed income contracts to minimise the potential for downside. We will be looking to reduce our exposure to this asset over the remainder of this year, and wait for a sell off before we increase back towards a normal allocation.

Commercial Property looks set to achieve income of 5% gross over the next 12 months, though the strength of the pound and Brexit negotiations will need watching closely. Inflows into property have picked up over recent months, and we may finally get a repricing to our property holdings this quarter which would give our portfolios a short-term welcome boost.

The biggest challenge we face is within our lower risk portfolios, where the defensive assets that support portfolios of this type look likely to produce very low returns after costs, and are no longer very defensive. We therefore need to be selective and importantly, our discretionary status means we are not tied to having to hold a specific allocation to a sector. If we don’t like it, we won’t buy it. The job of producing 3%-5% net per annum whilst limiting the downside, is still a real challenge, but we have the flexibility, team and process geared to help achieve it.

We are as always, absolutely committed to that challenge, and remain on course in 2017 to achieve this objective for our clients.