The Investment Committee

13th March, 2020

DB News

Coronavirus – Second Update from our Investment Team…

Please note that as a result of the current market turbulence, our Investment Team will be increasing the frequency of their communications to ensure clients are up-to-date and informed.

Global equity markets are in the middle of one of the most severe corrections in history. So far in 2020, the FTSE 100 (the UK’s most widely used equity benchmark) has fallen 28%. Many commentators are arguing that we are witnessing a repeat of the global financial crisis, and whilst this is not our central case, we have remained very defensive and alive to the possibility.

To start with, as we have said in previous blogs, the biggest challenge with the current outbreak is that we still don’t know enough about it. In some ways it is very similar to flu, and in other ways it isn’t. We don’t know if warm weather will offer relief, and we don’t know why some countries have had much worse outbreaks than others.

What we do know is that the number of cases is set to accelerate here, in Europe and in the US over the coming weeks. Governments as a result are starting to take more drastic action, following the lead of the Chinese who so far seemed to have successfully controlled their outbreak. But this action comes at an economic cost, with consumer spending and business confidence certain to take a big hit amidst the uncertainty. This is currently being priced into markets, hence the dramatic falls over recent weeks.

Our expectations at the start of this process was that markets would continue to fall in value, and as such we reduced our stock market exposure by around 30% across our cautious portfolios early into the sell off. We have benefitted as a result, given wider equity markets have continued to fall again this week, and our portfolios have provided resilient downside protection. As an example of the journey received, over the last 12 months our Low to Medium Portfolio has returned -2.19%, compared to the wider equity markets which have lost 23%.

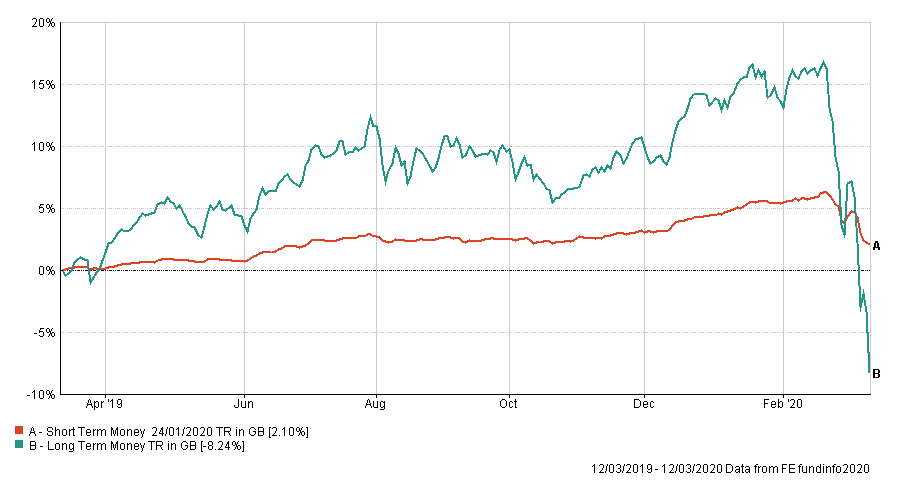

Digging a bit deeper, it’s important to remember that each of our portfolios contain both “short-term” and “long-term” assets. The short-term portion aims to achieve small returns but does not fall heavily in periods such as this. The long-term portion (equities) aims for long term growth but will be correlated in periods such as this. Again using the Low to Medium Portfolio as a benchmark, around 75% of this portfolio is in short-term assets, and 25% in long-term assets. As the chart below shows, the defensive portion has still provided a positive return over 12 months, reassuring clients that the majority of their portfolio is well protected, and diversified and flexible.

Digging a bit deeper, it’s important to remember that each of our portfolios contain both “short-term” and “long-term” assets. The short-term portion aims to achieve small returns but does not fall heavily in periods such as this. The long-term portion (equities) aims for long term growth but will be correlated in periods such as this. Again using the Low to Medium Portfolio as a benchmark, around 75% of this portfolio is in short-term assets, and 25% in long-term assets. As the chart below shows, the defensive portion has still provided a positive return over 12 months, reassuring clients that the majority of their portfolio is well protected, and diversified and flexible.

It is always disappointing to have a negative period for returns; however, it is important to retain perspective. We have worked through a number of significant market corrections over the last three decades, and in this case, whilst 2019 returns from our portfolios have been strong, values were stretched coming into 2020, and it was difficult to see where we would achieve a 3-4 % annual return without adding speculative risk. In the short term this correction has reduced our returns, however it has created a fantastic forward opportunity, as we believe over the longer term there is scope for returns, multiple times the 3% to 4% forecasted at the start of the year.

Therefore, forward strategy remains crucial. You won’t be surprised to know that we monitor markets for opportunities and threats on a daily basis. It is a challenging environment and is likely to remain so for the short term, however if we can continue to limit the downside versus the equity markets, the longer-term outlook improves markedly. Whilst it is not our expectation that things will drastically improve within the next few weeks, looking to 2021 and beyond we are now optimistic about the potential for strong returns.

Our forward approach is therefore to remain defensive in the short-term but look to identify good entry points to buy riskier assets at cheap prices. This action will ultimately lead to improved longer-term growth. There will doubtless be continued volatility, however when things improve (and they will), we expect the portfolios to rise with the upside to a greater extent than they have fallen with the downside, and that ultimately will lead to excellent returns further down the line.