Ashley Brooks

8th October, 2015

IC Insights

Investment Review Quarter 3 2015

Market Review of Quarter 3 2015

A torrid August ensured the summer holidays were not as relaxing as most investors had wished. Many of the business pages focussed on China, as markets worried about the effects of the slowing of a $10 trillion economy.

In a world where google analyses billions of pieces of data every day, it is difficult to understand why we cannot pinpoint the rate of Chinese growth. Their government would lead you to believe it is just under 7%, yet other indices, even that of the Chinese Premier, Li Keqiang, estimate it is closer to 2.5%. In fact, uncertainty has been a big feature of these summer months. Investors have speculated upon the timing of the first US interest rate rise, a landing range for the oil price, and a culmination of effects that imply slowing global growth.

Uncertainty breeds volatility, and indeed the VIX index; a measure of market volatility; is up over 20% over the quarter. Trends have been consistent though. Stock markets throughout the developed world have sold off significantly after a strong start to the year, with the UK market down more than most due to overexposure to commodity dependent companies. Bonds have benefited from a change towards a bleaker global outlook, and emerging markets remain under pressure. The only asset class that has remained relatively immune to the recent worries is UK commercial property, which has profited from the continued strength of the domestic economy.

Overall, it has have been a difficult quarter for investing money. In reality however, when markets fall, opportunity is created. It is crucial therefore, that when core investment markets fall significantly, our client portfolios preserve capital, relative to other markets. Our portfolios preserved capital in line with our expectations across all risk profiles, and as a result, unlike many multi asset portfolios that now sit on negative 12 month returns, all remain comfortably in positive territory. Our investment committees decision to reduce exposure to passive investments, and increase holdings in diverse asset selective positions have enabled our portfolios to weather the storm with very limited damage, and, although volatility will continue, there is now more value in some markets than there was three months ago.

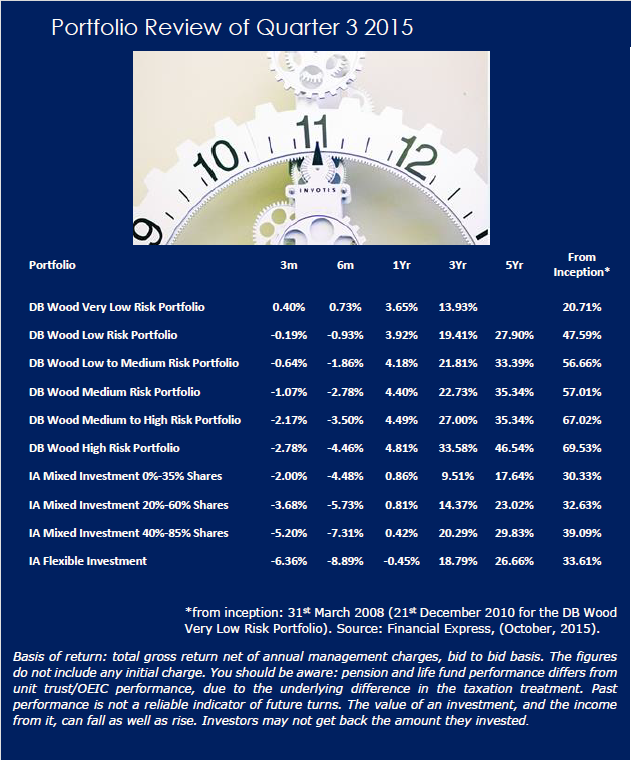

Portfolio Review

In absolute terms, our portfolios’ performance numbers are not outstanding. However, on a relative basis, the returns produced are compelling and demonstrate our ability to extract added value in difficult market conditions.

Focussing on the one year numbers, our portfolios have outperformed their benchmark by an average of 3.69%. You will note that in the main, this differential has occurred in the last quarter, where our capital preservation mandate has been very successful. Some of this excess performance can be attributed to our tactical moves; up-weighting commercial property and being more selective with our equity exposures in July is an example of this. However, our research also suggests that our fund selection ability has also been a key contributor, adding to performance and reducing risk in tandem.

In line with our cautious equity stance, we have specifically targeted funds that take less risk than the market, therefore reducing equity market losses. Our absolute return holdings have uncorrelated with most asset classes, diversifying our sources of return. Even our bond holdings, as light as they are, have added to performance numbers whilst reducing portfolio risk. Overall, it is the mix of assets and investment styles that we have used to our advantage.

It may seem contradictory, but it is not our aim to outperform our benchmarks. The benchmarks are of course important, as they are a measure of how we perform relative to the market average. In reality of course, our main aim is to provide consistent risk-adjusted returns that match our clients’ financial planning needs. Focussing on protecting the downside is a vital part of this, and our resilience to market falls has been highlighted by the quarterly numbers. Our key mandate has always been to operate with less risk than the core investment markets, and over the medium term, provide greater returns. You can see this demonstrated in the figures opposite. For your reference, our Low Risk Portfolio is benchmarked against the IM 0- 35% sector, Low to Medium and Medium versus the 20-60% sector, Medium High versus the 40-85% sector, and High versus the IA Flexible benchmark. Our Very Low portfolio is not benchmarked, as we run this as a cash alternative, it is designed to produce Bank of England base rate plus 3% over a 3 year cycle.

Market Outlook

Global factors have been at the forefront of investor’s minds over the last quarter, and with no domestic triggers on the horizon, this is likely to continue as a theme. There still remains a great deal of uncertainty, and this will mean continued volatility.

As long term investment managers, we are more concerned about the longer term outlook for China, and its effects on the global economy, than its current affairs. Such is the size of the economy, even if the rate of growth has slowed, China will still provide an important boost to the global economy. Still, its transition to a more consumer-based, western, economic model is likely to take some time, and with private sector debt at elevated levels, more downside in the short term could be possible. Unlike most western economies, China’s interest rates are not at historic lows, which gives them some room to manoeuvre if they need to boost the economy. The problem is that by doing so, China could force deflationary pressures on the rest of the world.

Sustained low inflation, and the aforementioned worries seem to have pushed back the interest rate tightening cycle further. It is now “December at the earliest” for the Federal Reserve, although it is unlikely that much will have changed between now and then. Therefore, unless we get a strong pickup in data from the US economy, and some inflation to match, it is more likely that interest rates stay at rock bottom levels until Q1 2016. For the UK, this could be pushed out further.

Closer to home, the UK economy should remain on track. Wage growth and the oil price fall will continue to enhance disposable income, which should transfer into more spending. European prospects have also picked up, which as our biggest trade partner, should in turn help the domestic economy.

Recent events have not facilitated changes to our portfolio strategy, but they have vindicated the cautious stance that we have held for some time. We continue to believe that equities, and risk assets in general, are the place to be over the longer term, but although more value has been created recently, there are too many headwinds to justify wholesale changes. Remain cautious and diligent, for now.

Investment Committee

*You should be aware that pension and life fund performance differs from unit trust/OEIC performance, due to the underlying tax treatment. Past performance is not a reliable indicator of future returns. The value of any investment can go up and down, and investors may get back less than they invested.*